MAKING the half-yearly monetary policy statement, State Bank Governor Shamshad Akhtar told a press conference last Thursday that the central bank will maintain its (tight) monetary policy stance while “effective administrative measures” are needed to control food prices.

MAKING the half-yearly monetary policy statement, State Bank Governor Shamshad Akhtar told a press conference last Thursday that the central bank will maintain its (tight) monetary policy stance while “effective administrative measures” are needed to control food prices.

The SBP appears to be saying it has done as much as it can to control inflation and it is now up to the government to take corrective measures on the administrative or supply-side to bring down food price inflation that has led to Pakistan's overall inflation rate to accelerate to a twelve-month high of 8.9 per cent in December. The Governor left the benchmark policy rate (3-day Repo Rate) unchanged at 9.5 per cent.

The monetary policy statement of the State Bank of Pakistan (SBP) makes two other important points: (a) inflation remains stubbornly high and is likely to exceed the 6.5 per cent target for the current fiscal year, and (b) the monetary policy continues to be supportive of the economic growth as threshold level of inflation for a stable economic growth. in the range of 4-6 per cent..

The assertion that Pakistan, being a developing country, needs a high inflation rate (6 per cent or so) to support a 6-8 per cent GDP growth is seriously questionable and is not supported by hard evidence from the most recent comparable GDP growth and inflation data of some major emerging markets as shown in graph 1.

Pakistan stands out with the highest inflation rate and the only country in the group whose inflation rate (8.9 per cent) is more than its GDP growth rate (6.6 per cent). This suggests that either there is something so unique about the structure of Pakistan’s economy that the divergence of its GDP growth and inflation data from the norm of even other developing and oil importing countries (leave aside those of the developed markets) has a valid and legitimate reason or the data itself is questionable.

Pakistan stands out with the highest inflation rate and the only country in the group whose inflation rate (8.9 per cent) is more than its GDP growth rate (6.6 per cent). This suggests that either there is something so unique about the structure of Pakistan’s economy that the divergence of its GDP growth and inflation data from the norm of even other developing and oil importing countries (leave aside those of the developed markets) has a valid and legitimate reason or the data itself is questionable.

However, even if we take data at its face value, the graph shows that most of these developing countries are growing at around six per cent or more while their inflation rate is around four per cent or thereabouts. The only exception is India whose inflation rate is 6.7 per cent but then its current GDP growth rate of 9.2 per cent is also significantly higher than Pakistan’s 6.6 per cent. The monetary policy statement does acknowledge that the inflation is relatively higher compared to its competitors and trading partners and this higher domestic inflation has offset the gains emanating from nominal depreciation of the rupee against other currencies. Is it making a case for an accelerated depreciation of rupee in the coming months because the monetary policy has failed to achieve the inflation target?

When most of major developing countries are recording healthy GDP growth while keeping overall inflation (this includes food and energy inflation) under five per cent, should not the government set five per cent inflation rate as target for the next fiscal year? This assumes additional significance - aside from domestic economy and political considerations in an election year - since the relatively higher inflation is hurting competitiveness and exports growth instead of supporting the declared policy objective of encouraging economic growth.

Still, it is fair to say that the SBP, primarily through open market operations and changes in the reserve ratios, has managed to bring down the overall growth rate in the private sector borrowings. Based on the monthly average loans outstanding of the scheduled banks, the loan growth during the six months to December 2006 was 14.5 per cent compared to 25.3 per cent growth during the previous year.

However, the impact of the overall tightening in the credit supply has been somewhat diluted by a Rs34.7 billion increase in loans under Long-term Financing for Export Oriented Projects (LTF-EOP) and R26.8 billion increase in loans under Export Finance Scheme (EFS), both offered at concessional or reduced rates.

The combined increase in loans under these financing schemes accounted for 54 per cent of the Reserve Money (M0) growth during the first half of the current fiscal year. Although there may be legitimate reasons for offering export financing at concessional rates, the reports about the abuse of such facilities abound with money being diverted to real estate and stock market investments. Such schemes can offset the benefits of a monetary tightening and derail the progress made in since late 2004. Given their large proportion in overall money supply growth, it is fair to argue that their rapid build-up may have adverse effects on the core function of the monetary policy, that is, achieving low inflation in the next 12-18 months.

Notwithstanding this, the impact of the monetary tightening is visible in rising interest rates and a deceleration in the principal indicator of the money supply, that is M2, during the first six months of FY2006-07. The three-month Karachi interbank offered rate (KIBOR) averaged 10.39 per cent during December 2006 compared to 8.98 per cent during January 2006. While raising interest rates is a perfectly legitimate response to building inflationary expectations, there is an other side to it.

Notwithstanding this, the impact of the monetary tightening is visible in rising interest rates and a deceleration in the principal indicator of the money supply, that is M2, during the first six months of FY2006-07. The three-month Karachi interbank offered rate (KIBOR) averaged 10.39 per cent during December 2006 compared to 8.98 per cent during January 2006. While raising interest rates is a perfectly legitimate response to building inflationary expectations, there is an other side to it.

If real interest rates, that is, nominal interest rates minus inflation, are higher compared to a country’s competitors, they can hurt growth, particularly exports. Some policy makers argue that the local businesses and industrialists should not just look at the lower nominal interest rates in India because Pakistan’s inflation rate is higher. Simple enough, but a comparison of the real interest rates between Pakistan and India reveals a somewhat different and more complex picture.

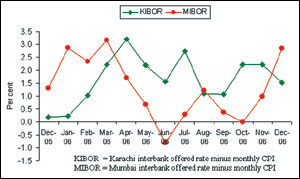

Graph 2 shows real interest rates in Pakistan and India. The monthly averages of 3-month KIBOR and 3-month MIBOR (Mumbai interbank offered rate) and monthly inflation (CPI) rates were used to calculate the real rates. The graph shows the real interest rates in Pakistan have stayed generally higher during 2006 compared to India’s. Although it is difficult to quantify the impact, higher real interest rates do contribute to higher cost of production and hurt international competitiveness.

Moreover, the data has some difficult implications from a monetary policy standpoint. The real interest rates in Pakistan depict a declining trend since mid-2006 while those in India show an upward trend.

Declining real interest rates can portend a higher inflationary environment 18 months down the road, as monetary tightening takes at least that long to make a dent in inflation. Here, it is relevant to note that the SBP’s last Thursday statement starts with a rather bold assertion that “monetary policy measures adopted in July 2006 augmented earlier tightening and reduced core inflation (Non-Food Non-Energy – NFNE) to 5.5 per cent by December 2006 from 7.4 per cent a year earlier.”

Given the widely accepted view, acknowledged even by the SBP Governor, that monetary policy takes 18 months or so to impact inflation rate; it is not clear how the July tightening has caused headline inflation to drop in just 6 months? While this may be excused as a statement made more for public consumption rather than on a serious note, more important issue is the recent and growing trend of emphasising core inflation as opposed to overall inflation that includes food inflation. Maybe it is just a better number to talk about because it looks good.

On the other hand, one may argue that core inflation is also followed closely in the developed economies such as the United States. However, there is a major difference between Pakistan’s inflation (CPI) measure and those of the developed world. Food inflation is the single largest component of Pakistan’s CPI and constitutes 40 per cent of this index compared to only 17 per cent or so in the U.S. and some other developed markets.

Together with energy, food inflation accounts for almost 48 per cent of the CPI or overall inflation in Pakistan. Therefore, in Pakistan’s context, core inflation (that is, Non-Food Non Energy inflation) is not as meaningful a measure as in some other developed countries. While supply-side factors do play a role in inflation, this should not detract the central bankers from targeting the overall inflation rate as the primary focus of the monetary policy. Monetary tools, such as margin requirements, do play a role in commodity financing and should be used appropriately to respond to the financing needs of essential items.

Moreover, while financial deregulation and innovation have made the money supply harder to interpret in the developed markets, domestic money supply control can be a relatively more effective tool of monetary policy in economies like Pakistan where private sector access to foreign borrowing and markets is fairly limited. The fact that a large sector of the economy is undocumented has little to do with the effect of money supply growth on inflation as has been well established in high inflation developing countries like Brazil and Turkey.

The SBP maintains it is capable of skilful management of the often difficult and complex objectives of meeting national growth priorities, liquidity and demand management, and controlling inflation. As central bankers around the world know too well from history, it is difficult to manage just one goal – low inflation – let alone many.

Given the propensity of the borrowers in Pakistan to abuse concessional credits and the difficulties in managing multiple and some times conflicting near-term policy objectives, the SBP will be better off to make achieving an inflation rate of five per cent or less as its core target for next 12-18 months. That by itself will facilitate growth and price stability. Failure to achieve low inflation will hurt growth and exports down the road as monetary policy mistakes can take up to 18-24 months to show up in even higher inflation numbers. But by then, elections will be over.

The writer is a former head of Emerging Markets Equity Investments, Citigroup.

information and the ban on X")

Dear visitor, the comments section is undergoing an overhaul and will return soon.